The gardening sector in France

The gardening sector in France – private sector

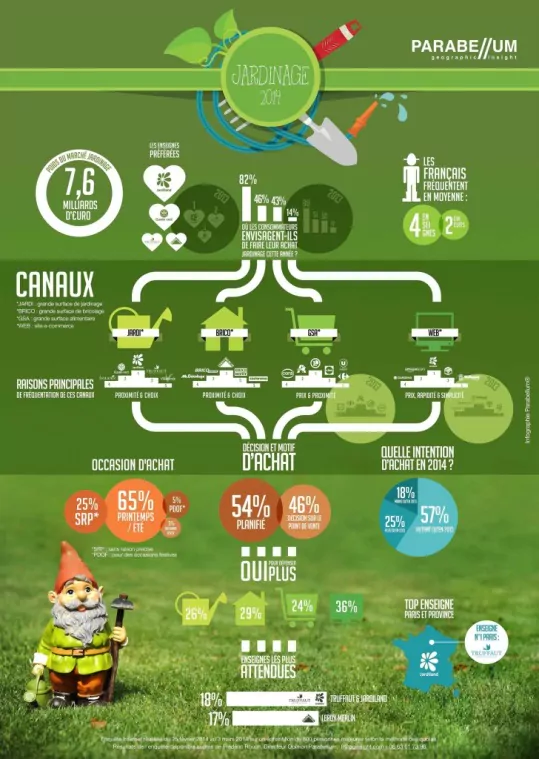

The gardening sector in France (private sector) accounted for €7.6 billion in 2014.

The gardening sector in France is a growing sector and presents various opportunities. Some key aspects are:

- Sustainability Trends: There is a growing interest in sustainable and eco-friendly gardening. Consumers are looking for products that are environmentally friendly, such as native plants, efficient irrigation systems and organic fertilisers.

- Increasing Green Space: With increasing urbanisation, many people are looking for ways to create green space in their homes, whether in gardens, on balconies or terraces. This has led to an increase in demand for plants, tools and gardening services.

- Gardening services: In addition to the sale of products, there is a growing demand for gardening services, such as garden design, maintenance and landscaping. Many people prefer to hire professionals to ensure that their green spaces are well cared for.

- E-commerce: Online sales of gardening products have grown significantly, especially after the pandemic. Online shops offer a wide range of products, from plants to tools and accessories.

- Events and Fairs: France hosts several gardening fairs and exhibitions, such as Jardins, Jardin and Salon du Végétal, where garden professionals can network and discover new trends and products.

- Education and Workshops: There is a growing interest in gardening education, with workshops and courses teaching people how to care for their gardens and grow their own plants.

Consumer habits in the gardening sector in France

The French consumer buys 82% of equipment in large garden centres (such as Gammevert, Jardiland, etc.) and prefers proximity and choice. In second place are the DIY superstores (such as Mr Bricolage, Leroy Merlin, etc.), with 46%, for the same reasons.

Supermarkets such as Leclerc, Super Uno or Auchan come in third place with 43%, mainly for price reasons, and finally the web with 14%, in commercial places, for its simplicity. In 54% of the cases, the purchase is already planned by the customer, and 65% of the time of purchase is in spring or summer. In 29% of cases, customers are willing to buy more than what they came to buy. The chains most visited by customers are Truffaut, Jardiland and Leroy Merlin.

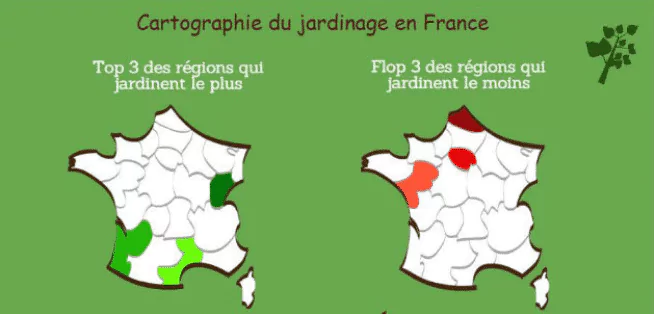

The areas where people are most passionate about gardening are Franche Comté, Languedoc Rosselló and Aquitaine. On the other hand, the least important gardening comes from Nord Calais, Ile de France and Pays de la Loire.

The distribution channels of the gardening sector in France

The gardening sector in France has recorded an average annual growth of 1% over the last decade. This overall performance highlights the disparities between distribution channels:

– Circuits that have been able to exploit promising market trends (development of environmental sensitivity, increased attention of the French to their garden, considered as a living room and where they invest) show above average growth. This is the case for garden centres which benefit from the dynamism of outdoor plants, develop in related segments and strengthen in green leisure and GSB which position themselves as multi-specialists in habitat / decoration;

– Other channels have below-average growth. GSAs are stagnating, penalised by a predominantly price-driven approach, a reduced offer and a deficit in the areas of supply and advisory/service development. Motorculture specialists have experienced a decline in sales in recent years as a result of the crisis.

Expansion and diversification of supply, modernisation of concepts

The challenges for dealers are:

- Improve the attendance rate of sales outlets. This requires an extension of the garden offer but also the opening in other universes (pet shop, decoration, outdoor recreation, even eating, textile…);

- Quickly adapt the offer to the effects of fashion and weather conditions;

- Attract novice gardeners by offering ready-to-use products so that the garden is not a constraint (kits, made-to-measure planters, etc.);

- Increase customer loyalty. Brands seek to establish an ‘expert’ positioning through advice (at the point of sale and via their website) and services (diagnostics, soil analysis, warranty, loading assistance, etc.);

- Offering attractive prices. In this perspective, white label development is an important strategic focus. This is especially so if low-cost struggles to impose themselves (see the failure of DockJardin), the GSA develops concepts dedicated to the garden (Jardi @E. Leclerc, Les Jardins d’Auchan) and Internet pure players (Cdiscount, Rue carries Commerce) position themselves on the market.

The concentration of the gardening sector in France

It is characterised by the great heterogeneity of chains and groups in terms of economic weight, network size and geographical coverage. This configuration favours a concentration movement, but operators will have to choose between internal or external growth to develop their network given the cost of these operations.

This movement should result in

– new reconciliations between central and independent networks (measurement effect, increased bargaining power);

– the absorption of some networks of insufficient size or regional scale;

– the rise of leading brands with an established reputation and sufficient financial margins to finance the development strategy;

– the decline in the number of independent centres and houses

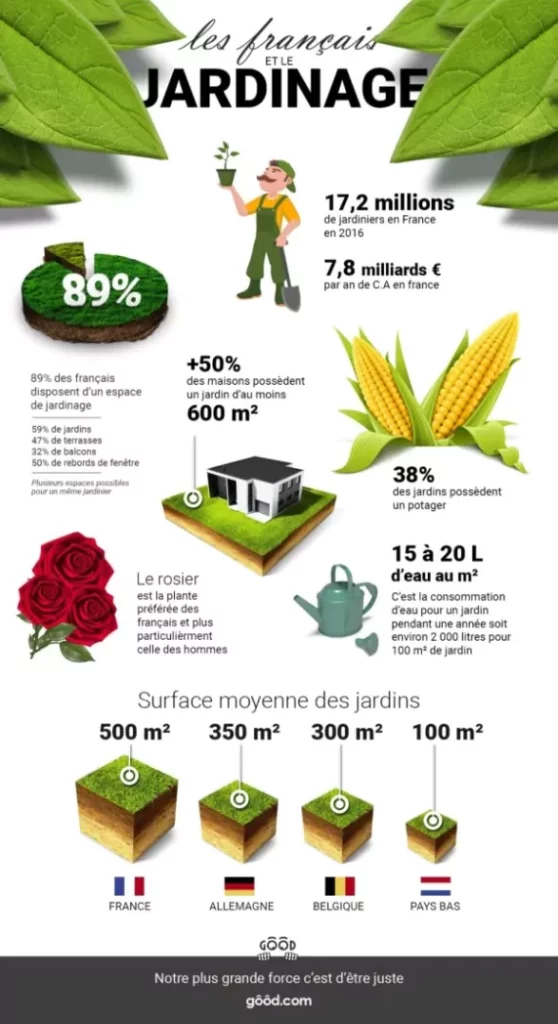

In France, 17.2 million people live in houses on a regular basis. More than half of the houses have a garden area of at least 600 m², and 89% of French people have a garden space at home. The average garden surface is the highest in Europe, with an average surface of 500 m².

Request our export service to enter the gardening sector in France.